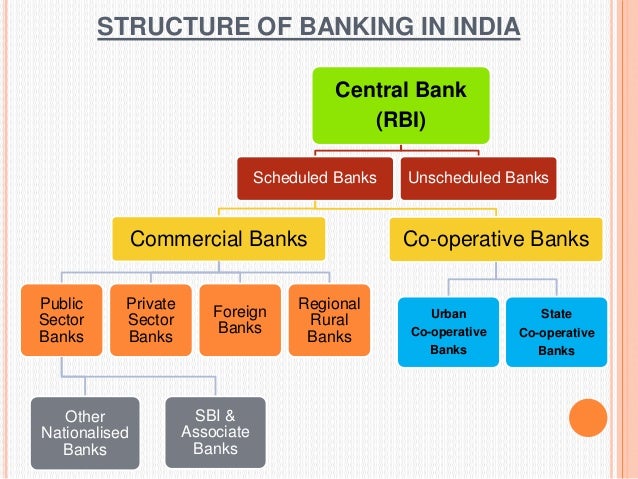

BANK

Bank: - Bank is a financial institution which accepts deposits and gives loan.

बैंक क्या है?

बैंक एक वित्तीय संस्थान है जिसे जमा प्राप्त करने और ऋण लेने के लिए लाइसेंस प्राप्त है। बैंक वित्तीय सेवाएं भी प्रदान कर सकते हैं, जैसे कि धन प्रबंधन, मुद्रा विनिमय और सुरक्षित जमा बॉक्स। दो प्रकार के बैंक हैं: वाणिज्यिक / खुदरा बैंक और निवेश बैंक।

Deposits:-

a. Current Account

b. Savings account

c. Fixed Deposit

d. Recurring deposit

जमा: -

a.। चालू खाता

b.। बचत खाता

c.। सावधि जमा

d.। आवर्ती जमा

Loans:-

a. Secured loan

b. Unsecured Loan

ऋण: -

ए। सुरक्षित कर्ज

ख। असुरक्षित ऋण

DEPOSITS खाता:

Current account:- Current account is an account with a bank or building society from which money may be withdrawn without notice, typically an active account catering for frequent deposits and withdrawals by cheque .

चालू खाता एक बैंक या बिल्डिंग सोसाइटी वाला खाता है जिसमें से बिना किसी नोटिस के पैसा निकाला जा सकता है, आमतौर पर चेक द्वारा बार-बार जमा और निकासी के लिए एक सक्रिय खाता।

Savings account:- Saving account is a deposit account held at a retail bank that pays interest but cannot be used directly as money in the narrow sense of a medium of exchange (for example, by writing a cheque). These accounts let customers set aside a portion of their liquid assets while earning a monetary return. In some jurisdictions, deposits in savings accounts do not incur reserve requirements.

बचत खाता: - बचत खाता एक खुदरा बैंक में रखा गया जमा खाता है जो ब्याज का भुगतान करता है लेकिन एक्सचेंज के माध्यम के संकीर्ण अर्थ में धन का उपयोग नहीं किया जा सकता है (उदाहरण के लिए, एक चेक लिखकर)। इन खातों ने ग्राहकों को मौद्रिक रिटर्न अर्जित करते हुए अपनी तरल संपत्ति के एक हिस्से को अलग करने दिया। कुछ न्यायालयों में, बचत खातों में जमा आरक्षित आवश्यकताओं को लागू नहीं करते हैं।

Fixed Deposits:- Fixed deposits are investment instruments offered by banks and non-banking financial companies, where you can deposit money for a higher rate of interest than savings accounts. You can deposit a lump sum of money in fixed deposits for a specific period, ranging from 7 days to 10 years.

फिक्स्ड डिपॉजिट्स: - फिक्स्ड डिपॉजिट बैंकों और गैर-बैंकिंग वित्तीय कंपनियों द्वारा दिए गए निवेश साधन हैं, जहां आप बचत खातों की तुलना में अधिक ब्याज दर के लिए पैसा जमा कर सकते हैं। आप एक निश्चित अवधि के लिए 7 दिन से लेकर 10 साल तक की एकमुश्त राशि जमा कर सकते हैं।

Recurring Deposit:- Recurring Deposit is a special kind of Term Deposit offered by banks in India which help people with regular incomes to deposit a fixed amount every month into their Recurring Deposit account and earn interest at the rate applicable to Fixed Deposits.

आवर्ती जमा: - आवर्ती जमा भारत में बैंकों द्वारा दी जाने वाली एक विशेष प्रकार की सावधि जमा है जो नियमित आय वाले लोगों को हर महीने एक निश्चित राशि को अपने आवर्ती जमा खाते में जमा करने में मदद करती है और फिक्स्ड डिपॉजिट पर लागू दर पर ब्याज कमाती है।

LOANS ऋण

Secured Loan:- Those loans are sanctioned against any security with bank

• Home Loan

• Vehicle Loan

• Property Loan

• Gold loan

सुरक्षित ऋण: - उन ऋणों को बैंक के साथ किसी भी सुरक्षा के खिलाफ स्वीकृत किया जाता है

• गृह ऋण

• वाहन ऋण

• संपत्ति ऋण

• गोल्ड लोन

Unsecured Loan:- These type of loans are sanctioned without any security only with the basis of customers income.

• Personal Loan

• Education Loan

• Business Loan

असुरक्षित ऋण: - इस प्रकार के ऋण केवल ग्राहकों की आय के आधार पर बिना किसी सुरक्षा के मंजूर किए जाते हैं।

व्यक्तिगत ऋण

शिक्षा ऋण

व्यवसाय ऋण

Third Party Products:-

• Mutual Fund

• Insurance

तृतीय पक्ष उत्पाद: -

• म्यूचुअल फंड

• बीमा

Thank you for reading my post. Kindly share this post to someone who need it. Share comment if you want any specific article.